Data that works harder

Buildings are quoted on hundreds of real data points, not just a handful — meaning insurers price less “unknown” and you get sharper, fairer premiums.

Find fair, data-backed cover with no hidden costs. Cohabit Insurance uses real building data to deliver smarter cover, clearer insights, and help lower the total cost of risk.

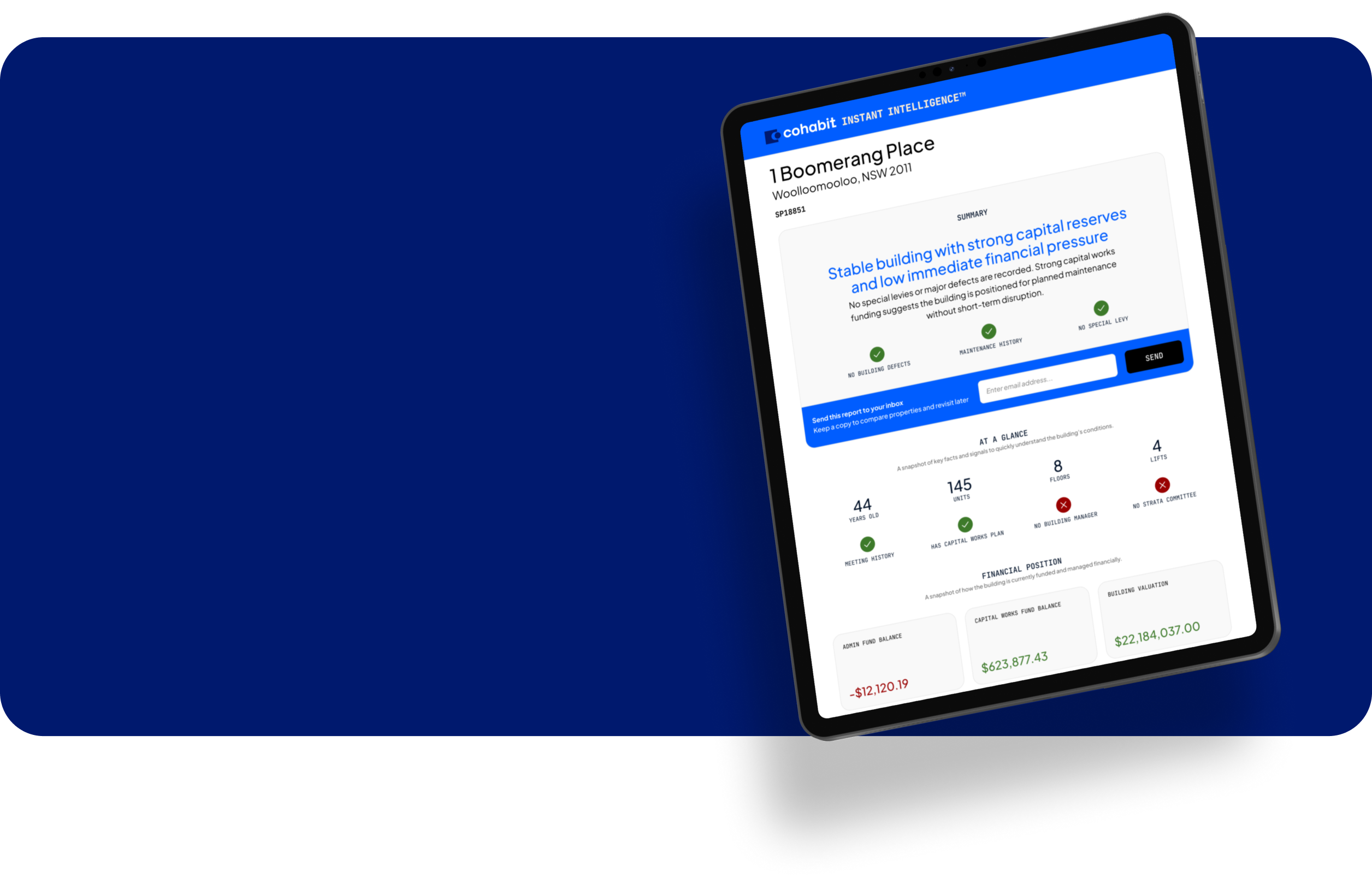

Most strata buildings are quoted on a handful of basic data points. Cohabit Insurance is different - we use 595+ real building data points to give underwriters a complete picture of your building, which means more accurate pricing, better coverage and fewer surprises at claim time.

Get In TouchOur insurance partners

Cohabit centralises strata records, inspections, insurance and building metadata — turning fragmented information into clear, structured profiles for every building in Australia.

Buildings are quoted on hundreds of real data points, not just a handful — meaning insurers price less “unknown” and you get sharper, fairer premiums.

A real-time claims portal and human specialists keep committees informed at every step based on your preferred level of visibility.

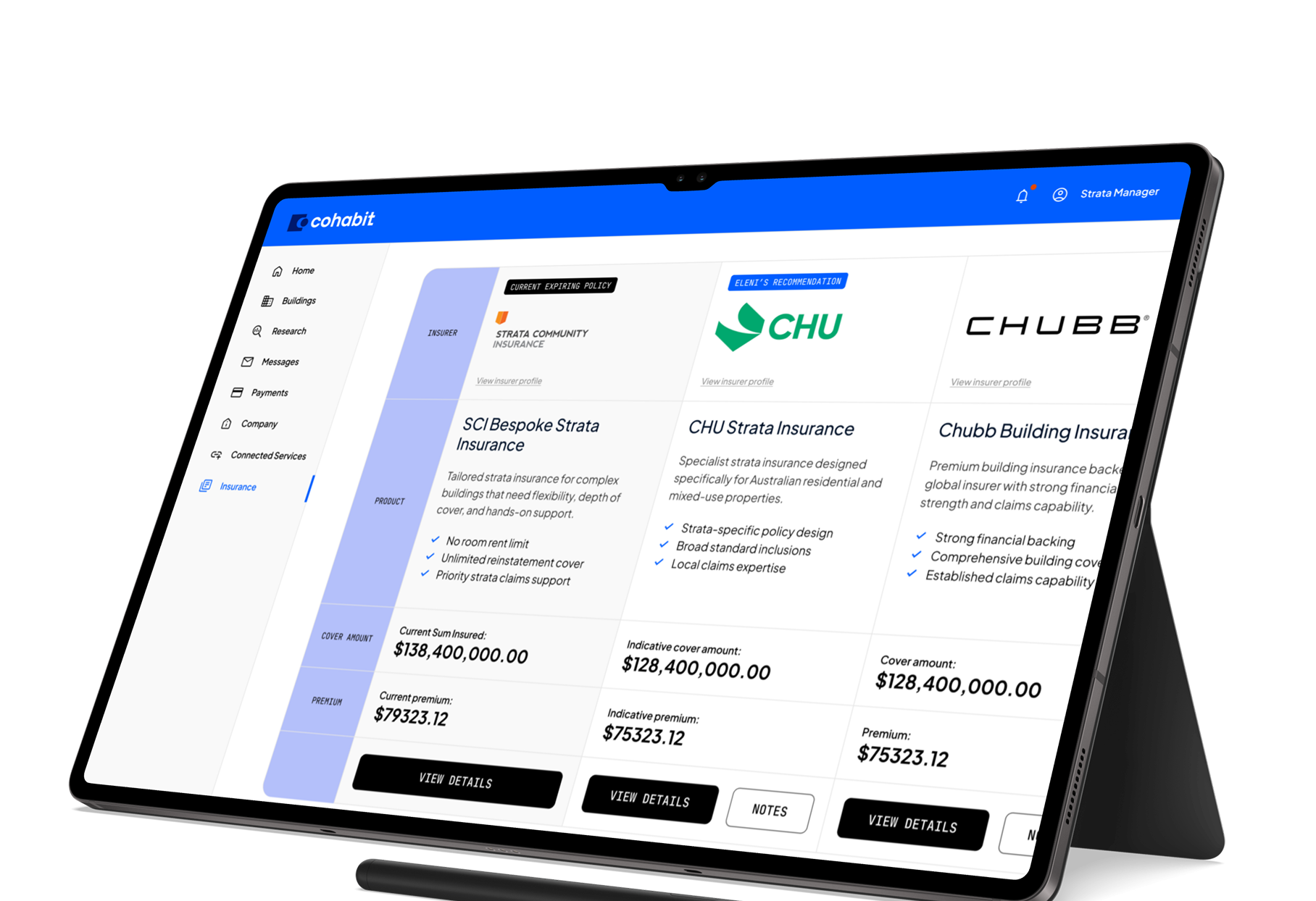

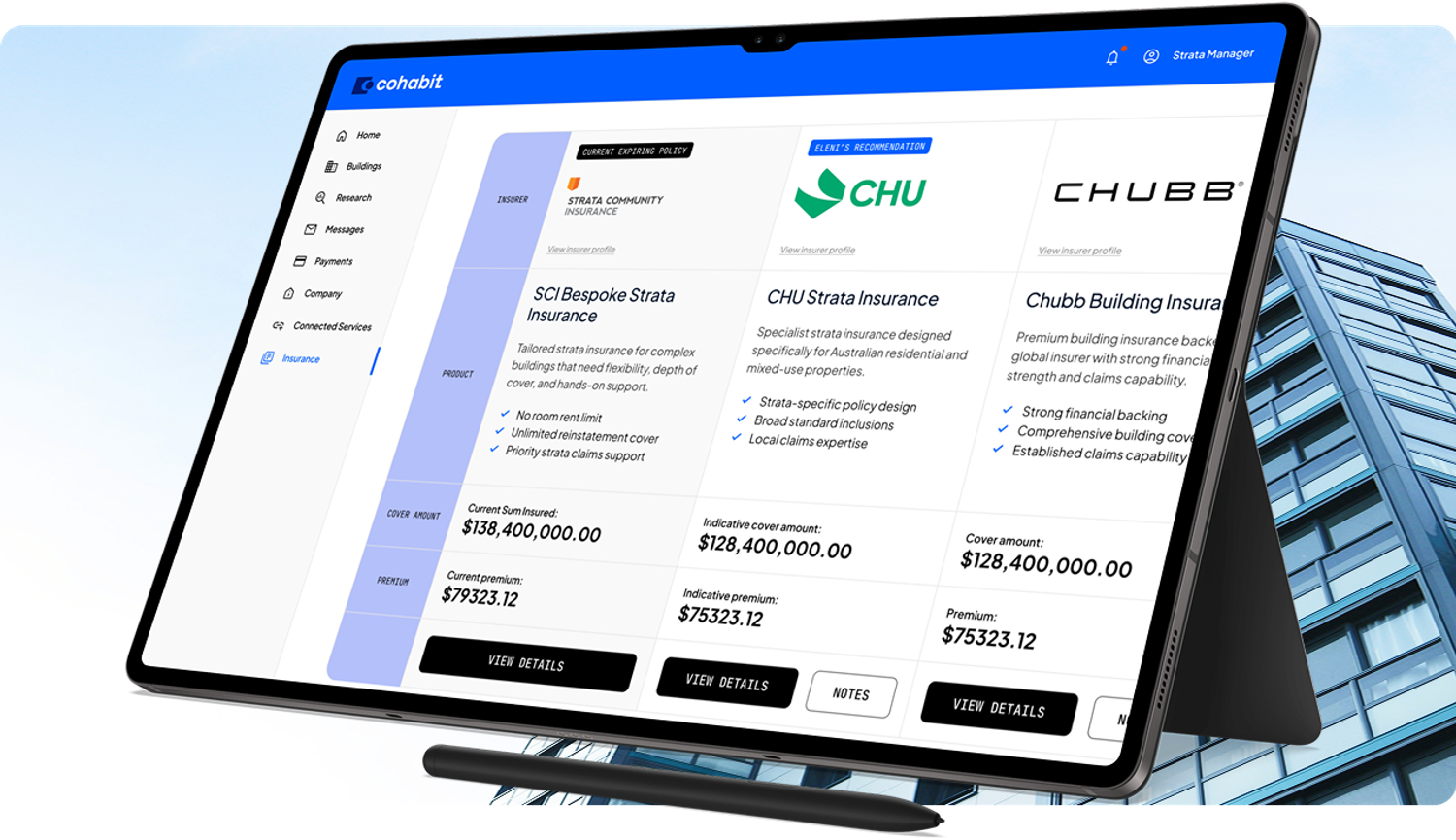

We quote with a panel of underwriters, including trusted strata insurers.

No hidden fees. Just transparent policy recommendations and understandable values.

Our team specialises in complex and high-defect buildings, including those with extensive defect schedules, regulatory compliance issues, or adverse claims history, as well as the placement of insurance for new developments.

Our private ownership allows us to provide objective, client-focused recommendations and structure a market strategy designed around your building's needs and outcomes.

We approach the entire market of underwriters and insurers, making sure you have the best chance of getting a competitive price. All proposals are presented clearly, enabling the Owners Corporation to make fully informed, confident decisions.

Every insurance program we design is bespoke. Coverage, limits, risk retention, and cost considerations are aligned to your building's construction, claims history, risk profile, and budget priorities.

We provide ongoing advice, practical claim support, and responsive communication, without generic call centre handoffs, ensuring issues are managed proactively throughout the policy period.

Our Insurance Director, Eleni Sivinos, specialises in managing complex, high-value placements with challenging underwriting profiles, drawing on experience across both domestic and international insurance markets. Her expertise enables her to navigate sophisticated risk scenarios and deliver tailored insurance solutions for clients with unique requirements. Eleni holds Tier 1 Insurance Broking and Tier 2 General Insurance qualifications, alongside a Bachelor of Laws and a Bachelor of Communications, reflecting a strong combination of technical insurance expertise, legal insight, and strategic negotiation skills.

(starting from 4 months prior to the renewal date)

(delivered ahead of decision time)

Simply complete the below form and one of our Strata Insurance Specialists will be in touch shortly.

Commonly asked insurance and claims-related questions.

For general FAQs go here

Yes, Strata insurance is mandatory in Australia for all residential and commercial strata titled properties. Strata titled buildings are legally required to hold insurance on the building, common property and liability protection.

a table.

It is strongly recommended that owner-occupiers, landlords, and tenants arrange their own insurance to cover risks specific to their individual lot, as these are not typically addressed under strata insurance.

Occupant Type Recommended Cover

Owner Occupied Personal Contents Insurance

Tenants Personal Contents Insurance

Landlords Landlord Insurance

Personal contents insurance provides protection for belongings such as furniture, jewellery, collections, and other valuable items.

Landlord insurance offers cover for risks associated with leasing a property, including liability arising from tenant occupancy, protection for landlord-owned contents, loss of rental income due to insured events, and a range of additional benefits.

Insurance requirements vary across each state and territory in Australia, however, all strata-titled properties are legally required to maintain a minimum level of insurance cover.

Policy Section

NSW

VIC

QLD

SA

WA

ACT

TAS

NT

Insured Property

M

M

M

M

M

M

M

M

Liability to Others

M

M

M

M

M

M

M

M

Voluntary Workers

M

OPT

OPT

OPT

OPT

OPT

OPT

OPT

Workers Compensation*

M

M

M

M

M

M

M

M

Fidelity Guarantee

OPT

OPT

OPT

OPT

OPT

OPT

OPT

OPT

Office Bearers Liability

OPT

OPT

OPT

OPT

OPT

OPT

OPT

OPT

Machinery Breakdown

OPT

OPT

OPT

OPT

OPT

OPT

OPT

OPT

Catastrophe Cover

OPT

OPT

OPT

OPT

OPT

OPT

OPT

OPT

WHS, Audit Costs & Legal Defence

OPT

OPT

OPT

OPT

OPT

OPT

OPT

OPT

Lot Owners’ Fixtures & Improvements

OPT

OPT

OPT

OPT

OPT

OPT

OPT

OPT

* Workers Compensation is mandatory in all jurisdictions where the body corporate employs workers. The definitions of “worker” and “employment” may vary between jurisdictions.

Under applicable legislation, Owner Corporations and Body Corporates are required to insure buildings for their full rebuild and/or replacement value. While a formal valuation by a qualified valuer is typically mandated every three to five years, it is considered best practice to review the sum insured regularly and obtain updated valuations every two to three years to account for rising construction costs and inflation.

If you didn't find your answer, feel free to reach out

Yes. You may enquire about coverage before lodging a claim. Your broker can provide factual references from the Product Disclosure Statement, and the insurer will give guidance without discouraging you from proceeding with a claim.

The insurer will outline the claims process, applicable excess, any waiting or exclusion periods, and how to contact them regarding your claim.

Within 10 business days of receiving your claim, the insurer will request any required information, appoint a loss assessor or adjuster if necessary, and provide an estimated decision timeframe.

You will receive progress updates at least every 20 business days. Routine enquiries will be responded to within 10 business days.

External experts are expected to provide a report within 12 weeks. If delays occur, the insurer will keep you informed.

If you didn't find your answer, feel free to reach out

The latest insights on strata buildings, insurance and the broader property market.

Without the right cover in place, landlords may face the risk of being exposed.

More

Underinsurance is becoming an increasing concern across the property and strata sector.

More

Data is transforming strata broking from a reactive process of policy placement into a proactive discipline centred on risk management and strategic advice.

More